How I Survived a Debt Crisis Without Losing My Mind

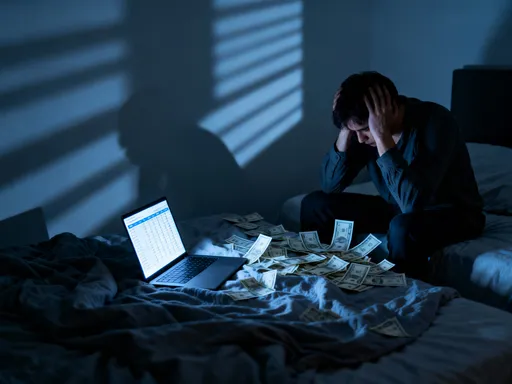

I remember staring at my bills one night, heart racing, realizing I couldn’t remember the last time I paid off a balance. The debt kept piling up, and I felt trapped. My minimum payments were barely making a dent, and every month felt like running on a treadmill—exhausting, but going nowhere. If you're in the same boat, you're not alone. Millions of households face the quiet crisis of mounting debt, often not from one big mistake, but from a thousand small oversights. This is the real talk—no fluff, no fake hacks—just the systematic cost control methods that pulled me back from the edge. Let’s walk through what actually works when your finances are spiraling, how to regain control without sacrificing your peace, and why long-term stability starts with intention, not willpower.

The Breaking Point: When Debt Stops Being Manageable

There’s a moment—often quiet, never dramatic—when debt stops being a number and becomes a presence. It sits in the back of your mind during dinner, whispers during your child’s bedtime story, and pulses in your chest when the phone rings. For me, it was the credit card statement that pushed me over the edge. The total was more than I made in two months. I had been making the minimum payments, telling myself I was staying on top of things, but in reality, I was just feeding interest charges. The balance wasn’t shrinking; it was growing. I felt paralyzed, ashamed, and utterly alone, even though I now know how common this is.

What made it worse was the illusion of control. I wasn’t dining at five-star restaurants or flying first class. My overspending was subtle: online shopping sprees after a long day, automatic renewals I forgot to cancel, eating out because I was too tired to cook. These weren’t reckless choices—they were habits, small leaks that turned into a flood. And because they didn’t feel excessive, I didn’t see the danger until I was drowning. The emotional toll was just as heavy as the financial one. I started avoiding my mailbox, dreading phone calls from unknown numbers, and feeling a constant undercurrent of anxiety that I tried to hide from my family.

That’s when I realized quick fixes wouldn’t work. Cutting out coffee wasn’t going to erase thousands in debt. I needed a real system—one that addressed not just what I was spending, but why, when, and how. I needed structure, not shame. This wasn’t about punishment; it was about protection. I had to stop reacting to money and start managing it with intention. The first step wasn’t budgeting—it was admitting I couldn’t wing it anymore. I had to treat my finances like a household project that needed planning, tools, and consistency. And that meant moving beyond guilt and into strategy.

Rethinking Cost Control: Beyond Just Cutting Coffee Runs

Most financial advice reduces cost control to sacrifice: skip the latte, pack your lunch, cancel the streaming service. While these actions can help, they often miss the bigger picture. Real cost control isn’t about deprivation—it’s about redesign. It’s not a diet; it’s a lifestyle change. The truth is, cutting small luxuries might save $50 a month, but if you’re overspending $500 in hidden or recurring costs, you’re still moving backward. Lasting change comes from identifying and altering the structure of your spending, not just the surface.

Take subscriptions, for example. They’re designed to be forgotten. A $15 monthly app feels harmless, but most people have five or more running in the background—gym memberships they don’t use, software they no longer need, box deliveries that arrived once and never got canceled. These add up to hundreds per year, quietly draining your account. I discovered I was paying for three different photo storage services, two meditation apps, and a meal kit I tried once. By simply auditing and canceling what I didn’t use, I freed up over $80 a month—without changing my daily routine.

Then there are recurring bills—the ones that increase without your permission. Internet, phone, insurance. These are prime targets for negotiation. Many people don’t realize they can call their provider and ask for a better rate, especially if they’ve been a long-time customer. I called my internet company and mentioned I was considering switching to a competitor. Without hesitation, they offered me a discounted rate for the next 12 months. That single call saved me $30 a month, or $360 a year. It took less than ten minutes and required no new habits.

Hidden spending leaks are another silent culprit. These include convenience fees, overdraft charges, and automatic upsells. One month, I was hit with a $35 overdraft fee because a subscription renewed on a day I didn’t expect. That incident taught me to track not just how much I spend, but when. By mapping out all my recurring charges on a calendar, I could anticipate cash flow dips and adjust my spending accordingly. This kind of awareness transforms cost control from guesswork into a predictable system. It’s not about living with less—it’s about spending with purpose.

Building Your Financial Firewall: A Step-by-Step System

When your finances are unstable, every dollar feels vulnerable. That’s why you need a financial firewall—a set of rules and structures that protect your money from impulsive decisions and unexpected drains. Think of it like home security: you wouldn’t leave your doors unlocked just because you trust your neighborhood. Similarly, you shouldn’t leave your finances exposed just because you’re trying to be disciplined. Systems beat willpower every time.

The first layer of this firewall is categorizing your spending. I broke mine into three buckets: needs, flexible costs, and true luxuries. Needs are non-negotiables—rent, utilities, groceries, minimum debt payments. Flexible costs include things like dining out, clothing, and home supplies—necessary, but adjustable. True luxuries are non-essentials: vacations, premium subscriptions, gadgets. This simple framework helped me see where I had room to adjust without sacrificing stability.

Next, I set up spending alerts through my bank. Any transaction over $100 would trigger a text or email. This wasn’t about restriction—it was about awareness. It forced me to pause before making larger purchases, even if I had the funds. Over time, this created a habit of intentionality. I also opened a second checking account just for variable expenses. Each payday, I’d transfer a set amount into this account based on my flexible budget. Once it was empty, I stopped spending in that category until the next month. This prevented overspending in areas like groceries or entertainment, even when my main account had money.

Another rule I adopted was the 24-hour approval for non-essential purchases. Anything over $50 required a full day to think it over. I’d write it down, sleep on it, and reassess the next day. More than half the time, I decided against the purchase. This wasn’t about denying myself—it was about ensuring my spending reflected my values, not my emotions. These systems didn’t eliminate spending; they made it deliberate. And that shift—from reactive to proactive—was the foundation of my recovery.

The Power of Delayed Decisions: How Pausing Saves Money

Impulse spending is one of the most underestimated drivers of debt. It doesn’t come from big, planned purchases—it comes from small, emotional decisions made in moments of stress, boredom, or fatigue. I used to shop online after a long day at work. It felt like self-care, but it was really avoidance. A $70 sweater here, a $40 kitchen gadget there—none of it was catastrophic on its own, but together, they were eroding my financial foundation.

What changed was introducing a mandatory pause. I decided that any purchase over $30 required a 24-hour waiting period. No exceptions. At first, it felt restrictive, even silly. But within weeks, I noticed something powerful: most of the things I wanted to buy, I didn’t want the next day. The urgency faded. The emotional trigger passed. The sweater I thought I needed? I forgot about it. The blender I was convinced would change my life? I realized I already had one.

This simple rule did more than save money—it rebuilt my relationship with spending. I stopped seeing purchases as solutions to stress or boredom. Instead, I began to ask: Do I need this? Will it add lasting value? Can I wait? These questions created space between desire and action, and in that space, clarity emerged. I started redirecting that energy into better habits—reading, walking, calling a friend. The act of waiting didn’t feel like denial; it felt like respect—for my money, my goals, and my future.

Over six months, this practice saved me nearly $1,200 in avoidable spending. More importantly, it reduced financial regret. I stopped looking back at my statements with shame. Every purchase I made felt intentional, not impulsive. And that sense of control became its own reward. Delaying decisions didn’t make me frugal—it made me thoughtful. And in the long run, thoughtfulness is far more sustainable than willpower.

Income Mapping: Aligning Earnings with Debt Goals

Cost control is essential, but it’s only half the equation. To truly escape debt, you need to manage what comes in, not just what goes out. Most people operate on a ‘pay yourself last’ model: they pay bills, cover expenses, and whatever is left goes toward debt. The problem? There’s often nothing left. By the time you’ve covered the month’s costs, your debt payment gets shortchanged—or skipped.

I flipped this model. The moment my paycheck hit my account, the first transfer I made was toward my debt. Not the minimum—more than that. I treated it like a non-negotiable bill, just like rent or utilities. This is called income mapping: assigning every dollar a job before you have a chance to spend it. I automated this transfer so it happened instantly, removing the temptation to delay or rationalize.

This shift changed everything. Instead of hoping I’d have enough at the end of the month, I guaranteed it. Even if I had to cut back on flexible spending later, my debt payment was already taken care of. It created a sense of progress that motivated me to keep going. Seeing the balance drop faster than before made the effort feel worthwhile.

I also prioritized high-interest debt first—the avalanche method. By focusing extra payments on the card with the highest rate, I reduced the total interest paid over time. Some prefer the snowball method—paying off the smallest balances first for psychological wins—but I chose the one that saved the most money. Either approach works, as long as it’s consistent. The key is to align your income with your goals from day one, not as an afterthought.

Tracking Progress Without Obsession: The Balanced Approach

Monitoring your finances is crucial, but constant checking can lead to anxiety and burnout. I used to look at my accounts multiple times a day, refreshing the page, hoping to see a drop in my balance. When it didn’t move fast enough, I felt defeated. I was so focused on the number that I lost sight of the progress.

I learned to step back. Instead of daily monitoring, I scheduled a weekly 15-minute review. I’d check my total debt, compare it to the previous week, and note any major expenses. I also tracked two simple metrics: my debt reduction rate (how much I was paying down monthly) and my expense-to-income ratio (what percentage of my income was going out). These gave me a clear, objective picture without the emotional rollercoaster.

I also created a visual tracker—a simple bar chart on my fridge. Every month, I’d color in how much debt I’d paid off. Watching the bar shrink over time was incredibly motivating. It turned an abstract number into a tangible achievement. This balance between awareness and detachment kept me engaged without being consumed.

The goal isn’t to live in your budget—it’s to use it as a tool. You don’t need to track every penny, but you do need to know the big picture. When you review your progress regularly but calmly, you stay on course without burning out. This sustainable rhythm is what turns short-term effort into long-term success.

Staying Resilient: Avoiding Relapse After Progress

Getting out of debt is hard. Staying out is harder. Many people make progress, then slip back—not because of a crisis, but because of complacency. Once the pressure lifts, old habits creep in. I call it lifestyle inflation: as your financial situation improves, you start spending more—bigger groceries, nicer clothes, spontaneous trips. It feels like a reward, but without caution, it can restart the cycle.

After I paid off my credit cards, I had to resist the urge to celebrate with a shopping spree. Instead, I kept my spending baseline lean. I maintained my subscription audits, kept my spending alerts active, and continued my 24-hour rule. I also built a small emergency fund—just $500 at first, then $1,000. This buffer protected me from unexpected costs without needing to borrow.

I also set up long-term alerts. Every three months, I’d do a full financial check-in: review my budget, check for new subscriptions, reassess my goals. This kept me accountable even when the urgency faded. I reminded myself that cost control isn’t a phase—it’s a lifelong system. Just like brushing your teeth, it only works if you do it consistently.

Finally, I shifted my mindset from scarcity to stewardship. I stopped seeing money as something to survive on and started seeing it as something to manage wisely. This wasn’t about living with less—it was about living with purpose. The peace I gained wasn’t from having more money, but from knowing I was in control. And that, more than any number, was the real victory.